Company News: Green Street Expands Self-Storage and Real Assets Intelligence Platform with Acquisition of StorTrack.

UK & European PBSA Demand Outlook: Roundtable Takeaways

On 30 June 2026, Green Street’s Advisory Services team hosted a roundtable breakfast to discuss the outlook for the student housing sector in the UK and Europe. Attendees included a mix of institutional investors and operators with significant portfolio exposure across the UK and Europe.

Green Street and StudentCrowd opened the discussion with a deep dive into student flows and operating performance, before the conversation expanded to the wider room as attendees shared their own views on the sector.

A summary of Green Street’s opening remarks is provided below. Complete the form below to download the full presentation slides.

UK & Europe Screen Attractive in a Global Context

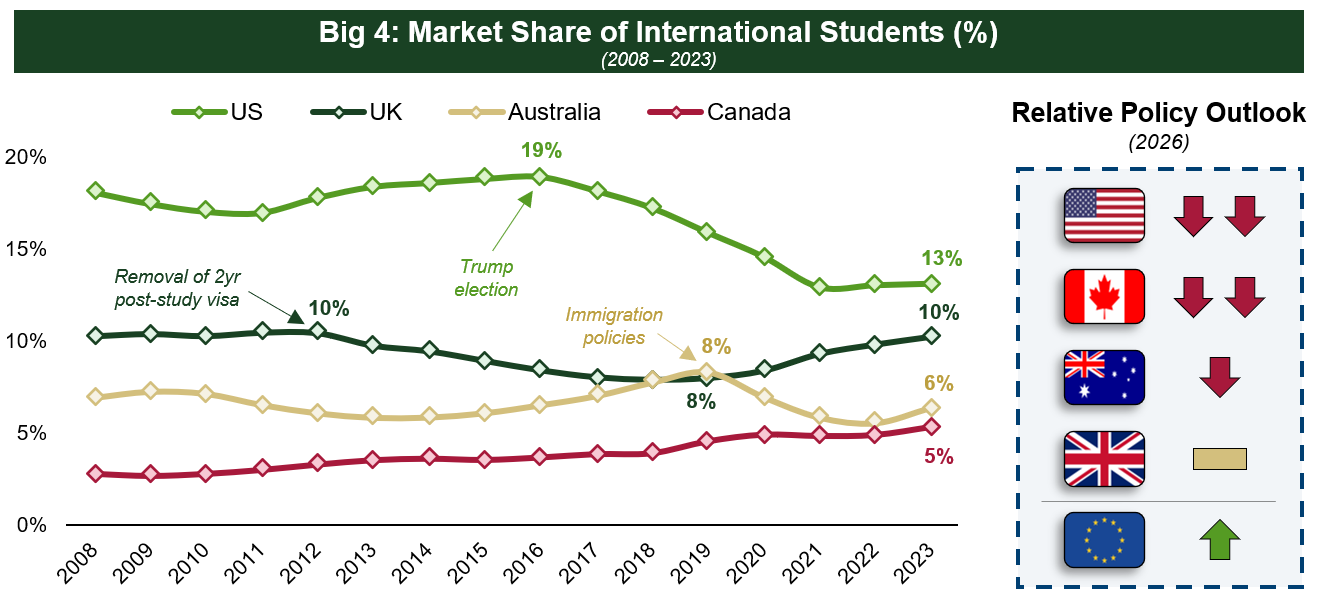

The global international student pool continues to grow, and countries’ ability to capture those students is heavily influenced by relative policy & sentiment (see Figure 1). Looking at policy outlook today, the UK and especially Europe screen positively vs. the US, Canada and Australia – all of which have seen a deterioration in policy & sentiment.

Early UCAS data suggest that application growth in the UK is strong for the upcoming 2026/27 academic year, with international growth driven by US & Chinese students. While up-to-date application data is less available on the Continent, several European countries screen favourably for PBSA investment based on relative policy, student-to-bed ratios and total demand pools.

Figure 1 — Big 4 Market Share of International Students (2008-2023) and Relative Policy Outlook (2026)

Bifurcation in Student Demand

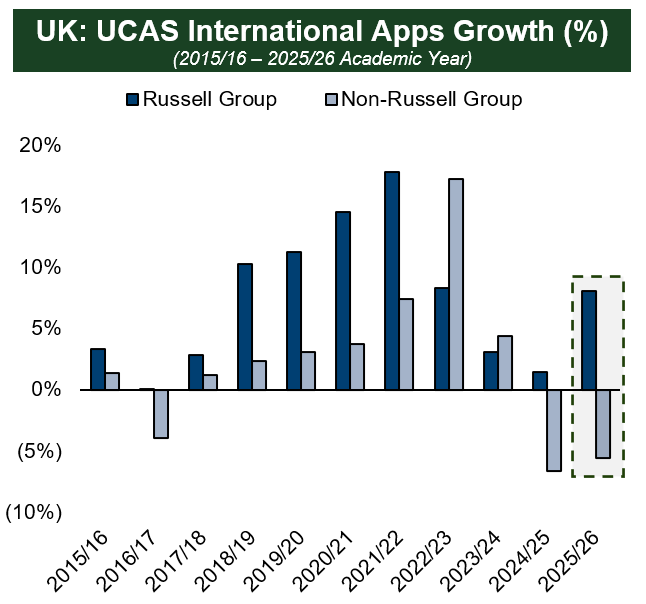

However, the recent growth in applications is not spread evenly. Highly-ranked universities are seeing outsized demand from international students (see Figure 2), both in the UK and in Europe, which concurs with asset-level occupancy trends for best-in-class assets.

Given the preference for quality, the “demand pool” – measured by application-to-acceptance ratio – for UK Russell Group (RG) universities has expanded significantly since Covid relative to non-RG where the ratio has declined. This deeper demand pool suggests top universities can better manage student intake & are less prone to sudden shocks. Living at home trends in domestic students also appear to be largely concentrated in the non-RG cohort, with RG students increasingly looking to PBSA as an accommodation choice.

Figure 2: UK UCAS International Applications Growth, Russell Group vs. Non-Russell Group (2015/16–2025/26)

Impact of Al and Weak Graduate Job Market

AI continues to remain a known unknown for future higher education demand. However, application data for the upcoming academic year suggests a more immediate potential impact on degree preferences: students are increasingly choosing STEM subjects (over non-STEM) and computer science apps are seeing a significant decline – presumably as AI has most directly affected software engineering jobs.

A weak entry-level job market and significant debt burden for graduates is also putting the attractiveness of higher education more generally into question. Near-term evidence suggests overall applications continue to rise, but medium- and long-term university participation rates could be under pressure.

Green Street Advisory Services works with institutional real estate investors on bespoke mandates, supporting with investment strategy, capital allocation, fundraising, and transactions. Contact our Advisory Services team to learn more.

Our TEAM

Andrew Simmons

Managing Director, Advisory Services

Green Street

Green Street

Andy joined Green Street’s European Advisory team in 2019 and has over 20 years of advisory experience, including 10 years focused on real estate. His experience is across all aspects of the capital structure: Mergers and acquisitions advisory (buy and sell side), equity fund-raising, and debt structuring – working with both listed and private clients to help them develop their growth strategies, identify investment opportunities and then raise the best-fit funding to implement the strategies. Prior to joining Green Street, Andy held roles within the Brookfield Group, Eurohypo, Ernst & Young and JC Rathbone Associates. Andy has an LL.B. (Law) from the University of Edinburgh and is a member of the Institute of Chartered Accountants of Scotland.

Samuel Charlton

Vice President, Advisory Services

Green Street

Green Street

Sam is a Vice President in Green Street’s Advisory Services group. He joined the firm in 2020 and helps support global real estate investors with investment strategy, capital allocation, transactions, and fundraising. Sam graduated with a Bachelor of Science in Accounting & Finance from the University of Warwick, and as part of his degree undertook an industrial placement in the Equities team at UBS Asset Management in London. Sam speaks French and has successfully passed his CFA Level 1 exam.

Green Street Advisors, LLC is a U.S. limited liability company doing business as Green Street. The US Advisory business unit at Green Street is a state registered investment adviser and only offers US Advisory services through our California location. While Green Street offers some regulated products and services, global Research, Data and Analytics products along with Green Street’s global News publications are not provided as an investment advisor nor in the capacity of a fiduciary. Our global organization maintains information barriers to ensure the independence of and distinction between our non-regulated and regulated businesses. This blog is not a product of Green Street Research.