Company News: Green Street Infrastructure Research Now Available. Expanding Market Coverage Across Infrastructure Debt, Transport, and Data Centers.

Checking In, Not Checking Out: Why Hotel Demand Endures in the Airbnb Era

Technological disruption has reshaped how we book travel – but the data suggests it has barely dented why we choose hotels.

Is European Hotel Demand Actually Under Threat from Short-Term Rentals?

No – and the data is unambiguous. The single most important fact about the tourist accommodation sector is that the pie keeps growing.

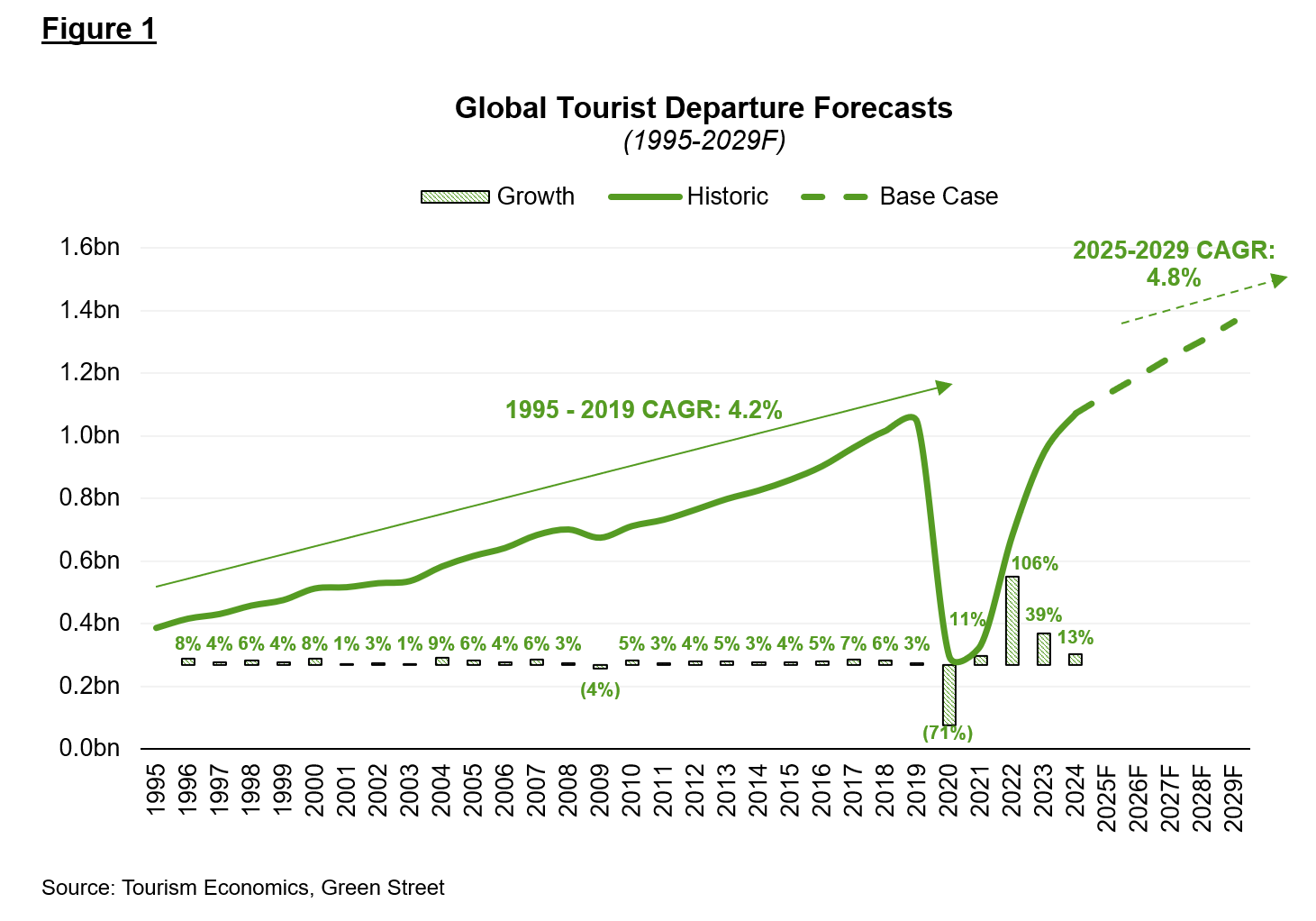

Global tourist departures have climbed from 0.4 billion in 1995 to roughly 1.1 billion in 2025, and we estimate this number could rise to 1.4bn by 2029 (Figure 1). Travel has proven remarkably resilient, recovering from financial crises and a global pandemic to set new records, driven by long-term growth in real GDP per capita across the world. When demand compounds at this pace, European hotel investment is not a zero-sum contest with short-term rentals (STR) such as Airbnb – there is room for both to grow.

Figure 1 — Global Tourist Departures, 1995–2029E. Source: Tourism Economics, Green Street.

Airbnb’s Extraordinary Supply Story

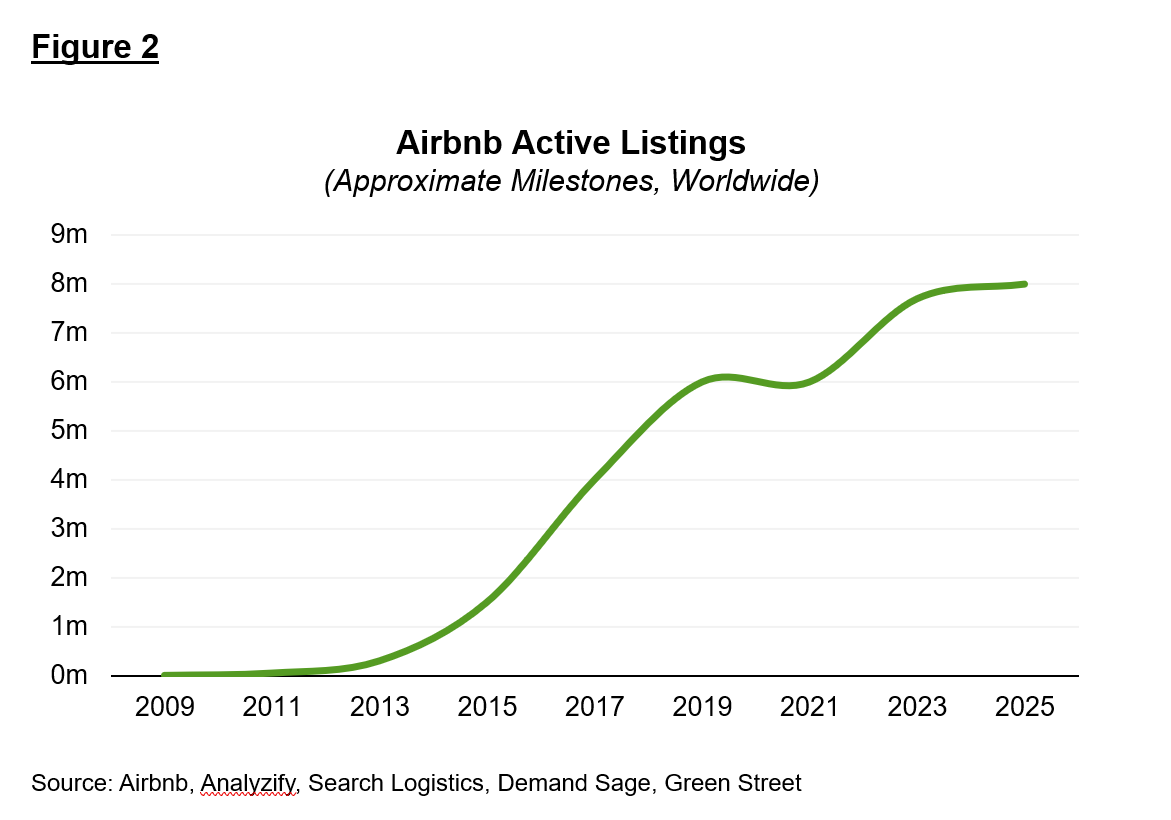

The concerns from hotel operators and investors about the threat from short-term rentals – particularly given growing questions over the depth of consumer travel wallets – are not unfounded. Airbnb’s growth has been astonishing. From air mattresses in a San Francisco apartment in 2008, the platform has scaled to more than 8 million active listings across 220+ countries (Figure 2), with over 5 million hosts and roughly 533 million nights and experiences booked in 2025 alone.

Figure 2 — Airbnb Active Listings Growth, 2008–2025. Source: Airbnb, Analyzify, Search Logistics, Demand Sage, Green Street.

No hotel chain in history has added inventory at anything like this rate. If short-term rentals were a straightforward substitute for hotels, supply growth of this magnitude should have visibly eroded the hotel sector’s share of demand. It has not…

The reason lies in who hotels and STRs actually serve. These are structurally distinct demand pools, not the same guests at different price points:

| Traveller segment | Primary accommodation | Why |

|---|---|---|

| Corporate & business travel | Hotels | Consistency, loyalty programmes, expensability, CBD proximity |

| Short-break urban stays | Hotels | Service, security, predictable quality standards |

| Extended leisure stays | Airbnb / STR | Space, kitchen access, neighbourhood experience |

| Group travel to non-urban destinations | Airbnb / STR | Cost per head, shared facilities, villa/cottage access |

In Europe the Share Shift Is Real, but Modest – and Older than Airbnb

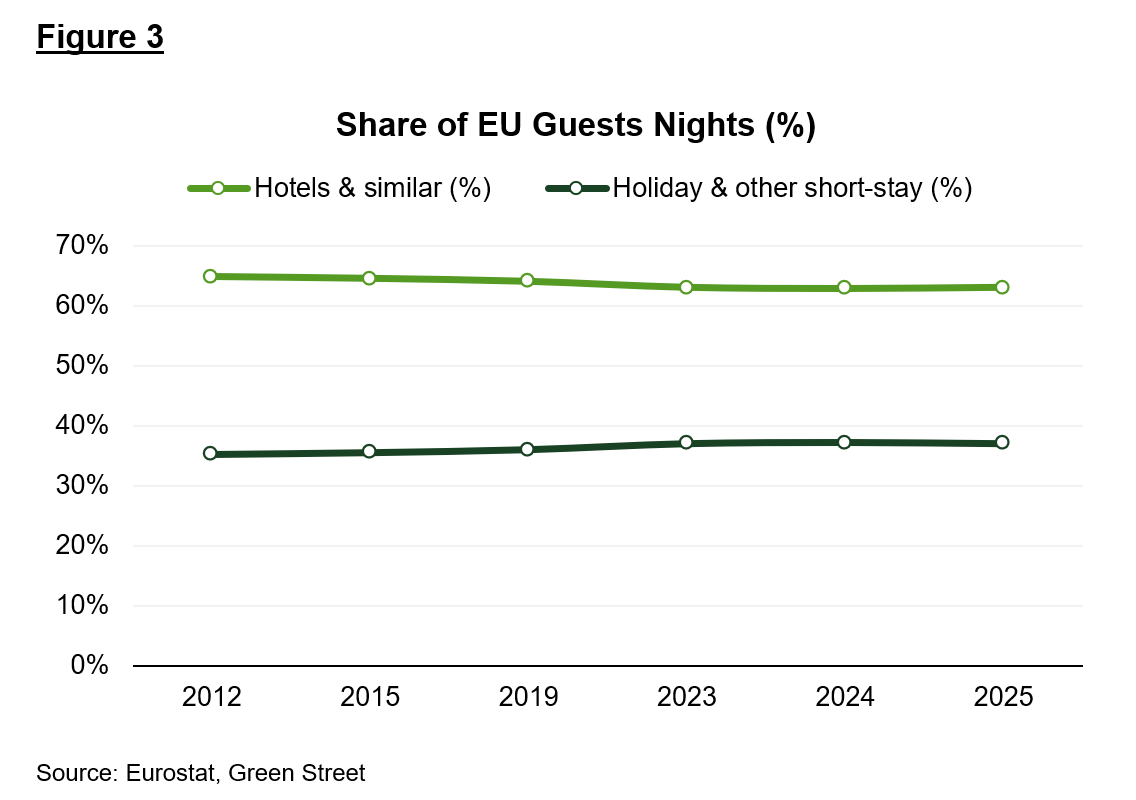

Eurostat guest-night data shows that “holiday and other short-stay accommodation” – rented apartments, holiday cottages, campsite accommodation and the like – was already an established segment in Europe long before Airbnb arrived, accounting for around a fifth of guest nights in the early 2010s. European travellers have rented villas in Tuscany and apartments on the Costa Brava for generations; Airbnb digitised an existing behaviour more than it created a new one.

Figure 3 — European Guest Nights by Accommodation Type. Source: Eurostat, Green Street.

Regulation Is Now Tilting the Field Back Towards Hotels

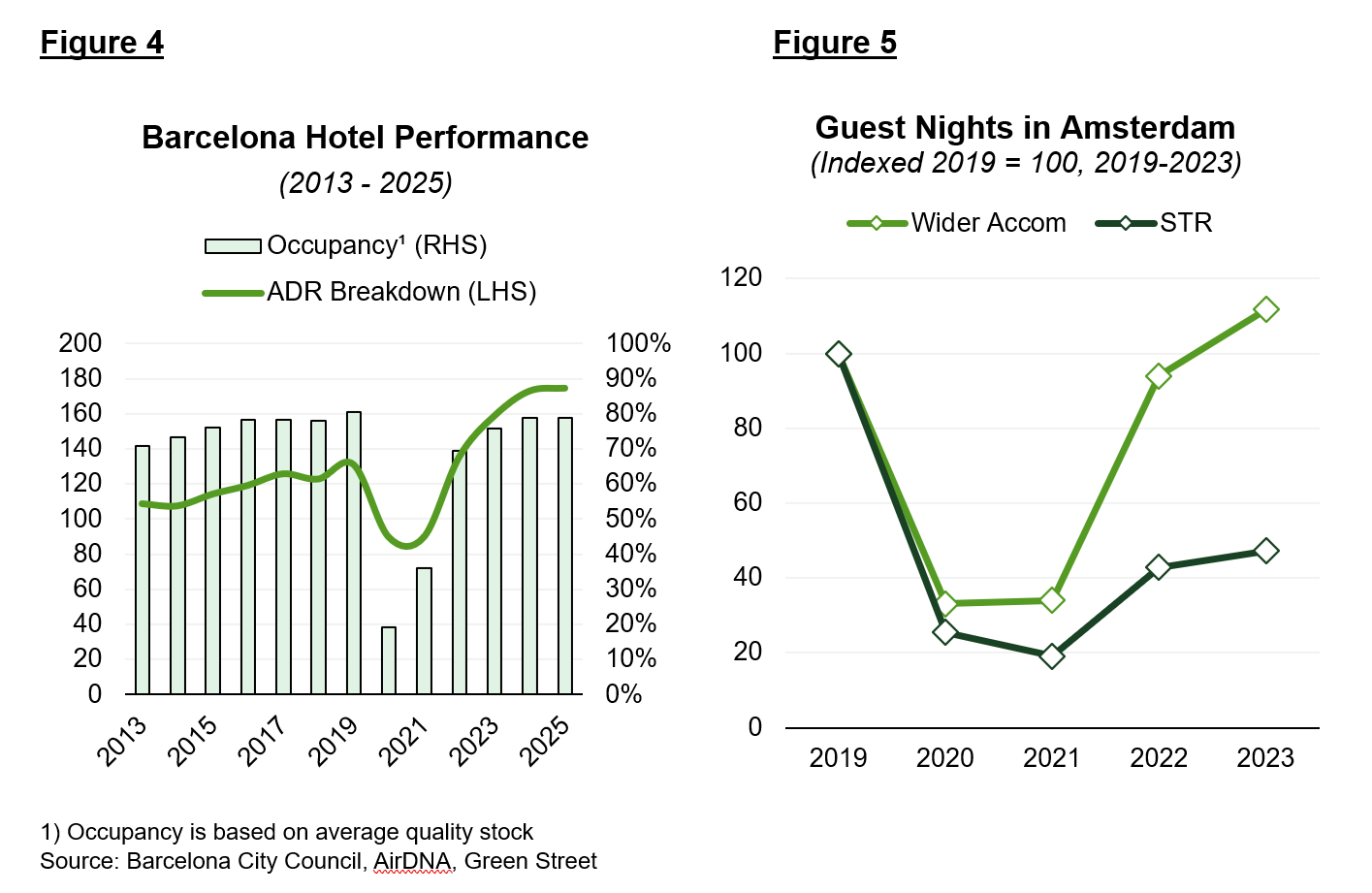

European cities are moving decisively against short-term rentals. Barcelona will not renew any of its ~10,000 tourist-apartment licences when they expire in November 2028, effectively phasing out the segment – despite hotel rates increasing by +60% since 2014 and occupancy levels remaining robust (Figure 4). Amsterdam caps holiday rentals of primary residences at 30 nights a year, with proposals to cut some zones to 15; the cap has resulted in stronger growth in non-STR accommodation post-Covid (Figure 5). Paris enforces a 90-night cap with heavy fines, Berlin restricts the “misuse” of housing, and Spain fined Airbnb €64 million in 2025 over unlicensed listings.

The regulatory picture across major European markets at a glance:

| City / Jurisdiction | Restriction | Status |

|---|---|---|

| Barcelona | No renewal of ~10,000 STR licences | Expires Nov 2028 |

| Amsterdam | 30-night annual cap; proposals to cut to 15 in some zones | In force |

| Paris | 90-night cap with heavy fines | In force |

| Berlin | Restrictions on residential housing misuse | In force |

| Spain | €64M Airbnb fine over unlicensed listings | 2025 |

| EU-wide | Reg 2024/1028: registration + platform data-sharing | From May 2026 |

Layered on top of this, EU Regulation 2024/1028 – applicable from May 2026 – mandates registration numbers and platform data-sharing, giving every city the tools to enforce its rules.

Figure 4 — Barcelona Hotel Occupancy and Rate Growth, 2014–2025 | Figure 5 — Amsterdam Non-STR Accommodation Growth Post-Covid . Note: Occupancy based on average quality stock. Source: Barcelona City Council, AirDNA, Green Street.

Hotels offer consistency, service, security and now growing regulatory certainty. Far from being disrupted into decline, European hotel investment looks set to remain the backbone of global travel.

Frequently Asked Questions

Does Airbnb actually reduce hotel occupancy in European cities?

Not materially – Eurostat data shows European hotel accommodation’s share of total guest nights has held steady since Airbnb reached scale on the continent. Hotels and STRs predominantly serve structurally distinct demand segments, which is why Airbnb’s supply growth has not translated into measurable hotel share loss.

Which European cities have the strictest short-term rental regulations?

Barcelona is the most restrictive, phasing out all ~10,000 licensed STR apartments from November 2028. Amsterdam enforces a 30-night annual cap with proposals to reduce to 15 nights in some zones. Paris has a 90-night cap with heavy fines. All are now backed by EU Regulation 2024/1028 from May 2026, which gives cities enforcement tools they previously lacked.

What does EU Regulation 2024/1028 mean for hotel investors?

EU Regulation 2024/1028, effective May 2026, requires STR platforms to share host registration data with local authorities – closing the enforcement gap that allowed unlicensed listings to persist despite local caps. For hotel investors, this means existing STR restrictions in European gateway cities will now be consistently enforceable, systematically constraining competing STR supply.

Arsalan Obaidullah

Vice President, Advisory Services

Arsalan joined Green Street’s Advisory & Consulting Group in 2021. He previously worked as a leading analyst on Morgan Stanley’s Equity Research team, covering European utilities, and at Deutsche Bank covering European capital goods. He also has five years of experience as a residential property developer in London, where he focused on small private-capital market projects. Arsalan holds a BSc in Economics from University College London and is Fellow of the Institute of Chartered Accountants in England and Wales.

Gin Chong

Vice President, Advisory Services

Gin is a Vice President in Green Street’s Advisory Services Group and joined the firm in 2021. Prior to Green Street, he held internships in corporate finance at Savills, valuations at Revantage, and transaction strategy at EY-Parthenon. Gin graduated with first class honours in BSc Economics from the University of Warwick.

Green Street Advisors, LLC is a U.S. limited liability company doing business as Green Street. The US Advisory business unit at Green Street is a state registered investment adviser and only offers US Advisory services through our California location. While Green Street offers some regulated products and services, global Research, Data and Analytics products along with Green Street’s global News publications are not provided as an investment advisor nor in the capacity of a fiduciary. Our global organization maintains information barriers to ensure the independence of and distinction between our non-regulated and regulated businesses. This blog is not a product of Green Street Research.